Medium-Duty Resilience Shines as Heavy-Duty Trucks See Sector Shifts

November’s medium- and heavy-duty truck market remained steady, shaped by seasonal trends, economic pressures, and key shifts across specific sectors.

December 11, 2024

The medium- and heavy-duty truck market displayed a mix of steady performance and sector-specific shifts in November.

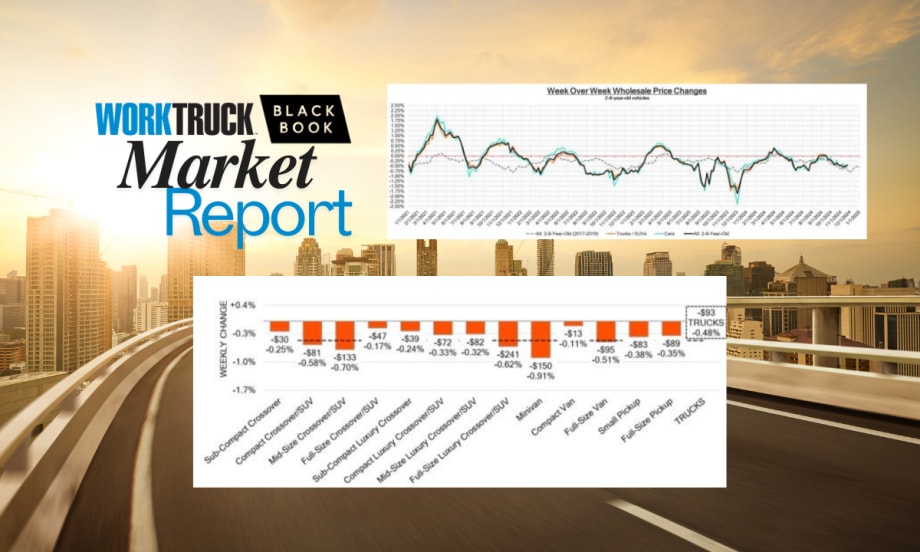

Photo: Work Truck | Black Book

3 min to read

As November wraps up, medium-duty and heavy-duty truck values highlight a blend of stability and sector-specific adjustments. Seasonal depreciation is easing compared to previous years, but careful monitoring remains key for fleet managers.

What does this mean for your work truck fleet?

November Week-By-Week Highlights

Week 1: November 5, 2024: Medium-duty trucks began the month with a marginal decline of 0.2%, aligning with seasonal expectations. Heavy-duty trucks showed mixed results, with over-the-road (OTR) models posting a 0.4% increase while construction trucks dipped slightly (-0.1%). Fleets remained focused on strategic purchases as interest rates continued to impact long-term decision-making.

Week 2: November 12, 2024: Medium-duty truck values remained relatively flat, while heavy-duty segments gained momentum. Regional tractors (HR) saw the most significant week-over-week increase at +0.6%, indicating steady demand in local operations. OTR trucks added another +0.5% gain, emphasizing resilience in long-haul applications.

Week 3: November 19, 2024: Heavy-duty sectors experienced another strong week, with regional tractors continuing their growth streak (+0.7%) and construction trucks reversing previous losses (+0.3%). Medium-duty trucks, however, faced a slight dip (-0.1%), marking a cautious pause amid fluctuating auction volumes.

Week 4: November 26, 2024: As the month closed, all eyes were on medium-duty trucks, which saw a minor rebound of +0.1%. Heavy-duty trucks remained a bright spot: OTR trucks gained +0.9%, their highest weekly increase in months, while regional tractors and construction trucks posted modest gains of +0.4% and +0.2%, respectively. Fleets sought opportunities in newer models, particularly 2022 and 2023 trucks, which outperformed older ones.

Key Market Trends: November Overview

The medium- and heavy-duty truck market displayed a mix of steady performance and sector-specific shifts in November.

While older medium-duty models saw slight depreciation, newer ones remained stable, reflecting improved year-to-date trends compared to 2023. Heavy-duty sectors showed varied movements, with newer models consistently demonstrating stronger value retention.

Here’s a closer look at the key trends:

Medium-Duty Trucks

For model years 2014 to 2021, medium-duty trucks experienced a slight wholesale value decrease of 0.2% from October to November. This contrasts with a 0.2% increase during the same period last year. Year-to-date, these models have depreciated by 12.1%, a notable improvement over the 23.3% depreciation observed in 2023.

2022–2023 medium-duty trucks held steady with no net change from October to November, following three months of increases exceeding 1.0%. Year-to-date depreciation for these newer models is just 0.7%, a sharp improvement compared to the 10.8% decline recorded in 2023.

Heavy-Duty Trucks

Sector trends varied:

Construction Trucks (HC): Older models saw a minor value decrease (-0.3%), contributing to a cumulative 17.6% depreciation this year.

Over-the-Road Trucks (OTR): Values increased 0.9% month-over-month, despite a 9.9% year-to-date decline.

Regional Tractors (HR): Experienced a 0.6% monthly increase, with a 5.9% year-to-date depreciation.

For 2022–2023 models, all three heavy-duty sectors reported value increases ranging from 0.5% to 1.5%, reflecting resilience in newer trucks.

Seizing Opportunities and Looking Ahead to 2025

Medium-duty trucks offer stability, while depreciation in heavy-duty models presents opportunities for cost-conscious acquisitions. Newer models have proven to hold their value better, making them a strategic choice.

As 2025 approaches, aligning purchasing strategies with these trends can keep your fleet competitive. Stay informed, evaluate inventory carefully, and make deliberate decisions to maximize your investments.

More Remarketing

AP Fleet Management Expands Remarketing Program for Commercial Work Trucks

AP Fleet Management expanded its commercial vehicle remarketing program with dedicated resale services and an online marketplace for used work trucks.

Read More →

REP Inspection Services Launches, Delivering Professional Equipment Inspections

REP Inspection Services, led by someone with more than 30 years of industry experience, has launched its professional inspection services for trucks, trailers, and equipment across the commercial vehicle industry.

Read More →

Introducing Work Truck’s 2025 Remarketing Report Series

Work Truck’s 2025 Remarketing Report Series uncovers how data, timing, and technology are reshaping resale value and driving smarter fleet strategies.

Read More →

Fleet Remarketing Outlook 2026: EVs, Policy, and the Power of People [Part 4]

From EVs to policy changes, the 2026 fleet remarketing outlook is all about people, progress, and finding opportunity in stability.

Read More →

Digital Fleet Remarketing: How Tech and Transparency Build Buyer Confidence [Part 3]

Technology and trust are reshaping fleet remarketing in 2025. See how data, transparency, and partnerships drive better resale outcomes.

Read More →

Fleet Replacement Strategy 2025: When to Hold and When to Fold [Part 2]

Knowing when to sell or hold is key in 2025. Discover how fleet professionals use data and TCO insights to make smarter remarketing calls.

Read More →

The 2025 Work Truck Remarketing Market: Prices, Pressure, and What Comes Next [Part 1]

Fleet remarketing in 2025 is stabilizing. Experts share how prices, rates, and new tech are shaping used truck values and resale strategies.

Read More →

Copart and One Inc. Partner to Improve Auto Claims Process

ChatGPT said: One Inc and Copart partner to speed up lienholder payments, helping insurers process total loss vehicle claims faster and improve customer experiences.

Read More →

Fleet Remarketing Industry Council Launches to Shape Future Resale Value

What if fleets could shape how their vehicles are valued after resale? Now they can.

Read More →

CAR Partners with NAFA Fleet Management Association For 2026 Event

The event will connect fleet managers with vehicle remarketers to delve into topics that help fleet operations find remarketing solutions.

Read More →