Three Ways to Reimburse Employees for EV Home Charging: The Good, the Bad, and the Ugly

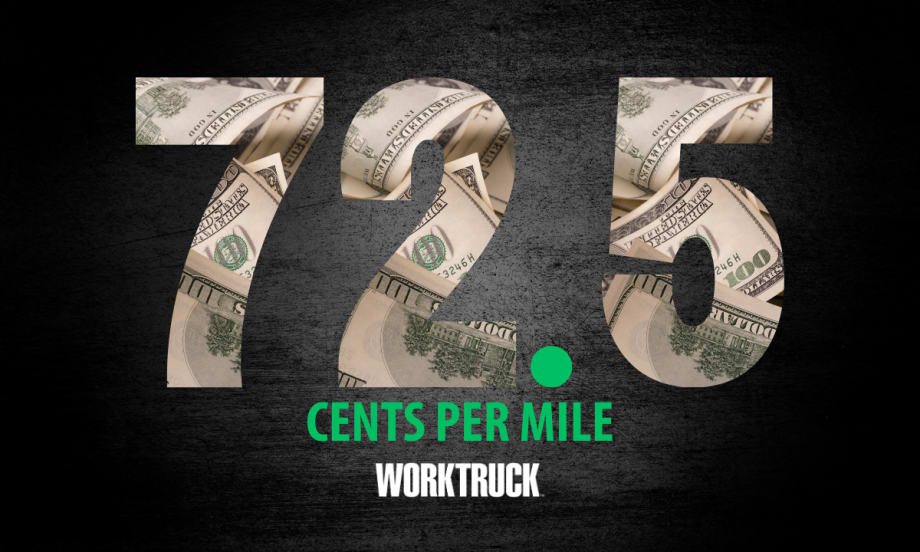

2026 IRS Business Standard Mileage Rate Rises to 72.5 Cents Per Mile

IRS boosts the 2026 business mileage rate to 72.5 cents per mile, up 2.5 cents. Here’s what it means for fleets and reimbursements.

January 6, 2026

The IRS set the 2026 standard mileage rate for business use at 72.5 cents per mile, effective Jan. 1, 2026, reflecting updated vehicle operating cost data.

Credit: Work Truck

3 min to read

The Internal Revenue Service has released the updated optional standard mileage rates for 2026, increasing the business rate to 72.5 cents per mile. The new rate goes into effect Jan. 1, 2026, and applies to the use of cars, vans, pickups, and panel trucks, including fully electric and hybrid vehicles, as well as gas and diesel-powered models.

What are the 2026 Standard Mileage Rates?

Beginning Jan. 1, 2026, the IRS mileage rates are:

72.5 cents per mile driven for business use (up 2.5 cents from 2025)

20.5 cents per mile driven for medical purposes (down 0.5 cents from 2025)

20.5 cents per mile driven for moving purposes for certain active-duty military members and certain members of the intelligence community (down 0.5 cents from 2025)

14 cents per mile driven in service of charitable organizations (unchanged)

The IRS notes the business mileage rate is based on an annual study of fixed and variable costs, while the medical and moving rates are based on variable costs only. The charitable rate is set by statute.

Why the Mileage Rate Matters for Fleets and Employers

For companies reimbursing drivers who use personal vehicles for work, the IRS mileage rate is often used as a benchmark because it helps define the tax-free reimbursement ceiling for mileage-based plans. Employees and eligible taxpayers may also use it to calculate deductible vehicle costs, depending on their situation.

To put the change into perspective, a driver logging 10,000 business miles per year would see reimbursement rise by about $250 versus 2025, if reimbursed at the standard rate.

Motus, a vehicle reimbursement provider, said the increase reflects rising ownership costs even as fuel prices cooled in 2025. According to Motus, factors such as vehicle prices, insurance, maintenance, and depreciation continue to drive the cost of operating a vehicle for work.

Standard Rate vs. Actual Expenses

The IRS reminds taxpayers that the standard mileage rate is optional. Taxpayers may instead choose to calculate the actual costs of using their vehicle.

However, taxpayers using the standard mileage rate for a vehicle they own and use for business must choose to use the rate in the first year the automobile is available for business use. In later years, they can choose to use the standard mileage rate or actual expenses.

For a leased vehicle, taxpayers using the standard mileage rate must employ that method for the entire lease period, including renewals.

A Few Other Details Fleets May Want to Note

Notice 2026-10 also includes updates relevant to reimbursement and employer-provided vehicle programs. The IRS set the depreciation portion of the business mileage rate at 35 cents per mile for 2026, used when calculating basis reductions under the standard mileage method.

The notice also sets a $61,700 cap on the vehicle value used for certain reimbursement and valuation rules, including FAVR plans and employer-provided vehicle valuation methods such as the cents-per-mile rule and fleet-average valuation rule.

More details are included in Notice 2026-10, which also outlines maximum automobile cost and employer-provided vehicle valuation rules for 2026.

More Operations

Sponsored•August 1, 2026

Top 50 Executive Fleets

It is that time of year again! Time for the 2026 list of the Top 50 Executive Fleets, presented by Automotive Fleet and Volvo as part of its annual Fleet 500. Download now to see this year's list of companies!

Read More →

Behind the Scenes: Building the Ringmaster of the Road from Body to Paint Part 2

The body is built, the paint is on, and Team Fletcher’s Soap Box Derby car is nearly ready for testing ahead of race day in Akron.

Read More →

It's All Downhill from Here! Fleet Industry Raises $22,000 for Skilled Trades Scholarships

Work Truck’s Lauren Fletcher and Automotive Fleet’s Chris Brown turned a friendly racing rivalry into $22,000 for automotive technology and skilled trades scholarships.

Read More →

Fleet Confidence, Safety, and Smarter Risk Management Lead This Month

This month’s TruckChat: Top Monthly News Recap explores what it takes to build confidence across a fleet, from stronger leadership and technician support to better safety preparation, smarter use of telematics, and clearer plans for when something goes wrong.

Read More →

From Fleet Operator to OEM Leader: Tina Kourakos’ Career Lessons

Tina Kourakos shares the lessons, relationships, and career pivots that shaped more than 30 years in fleet, plus the advice every new fleet manager should hear.

Read More →

WEX Brings Standard Fleet's Connected Vehicle Platform to Fleet Customers

This week’s product launch with Standard Fleet’s connected vehicle platform reflects WEX Venture Capital's strategy of turning startup innovation into customer solutions. Standard Fleet is now available to WEX fleet customers.

Read More →

Meet Atlas: Motive's AI Assistant for Fleets

Artificial intelligence is becoming a practical tool for fleet operations. In this video, Emily Parsons introduces Atlas, Motive's AI-powered assistant that combines conversational search with the ability to perform actions across the Motive platform.

Read More →

Sponsored•July 23, 2026

The Top 300 Commercial Fleets

The Top 300 Commercial Fleets: See the List

Read More →

NTEA Releases Updated Federal Excise Tax Guide for the Work Truck Industry

NTEA’s latest revised edition of its Federal Excise Tax Guide for the Work Truck Industry is now available to help fleet leaders navigate complex federal tax requirements.

Read More →

Super Dispatch Powers Centralized Vehicle Transport Operations for Merchants Fleet

Merchants Fleet has replaced fragmented transportation processes with Super Dispatch’s unified, API-powered platform to improve visibility, automation, and carrier performance.

Read More →