How New Green Laws Will Affect Medium-Duty Market

It is predicted that the medium-duty truck market will coast through 2024, and then accelerates as new emissions standards loom into 2025.

Near-term forecasts of demand and growth for Class 5-8 commercial vehicles in North America.

Photo: Work Truck

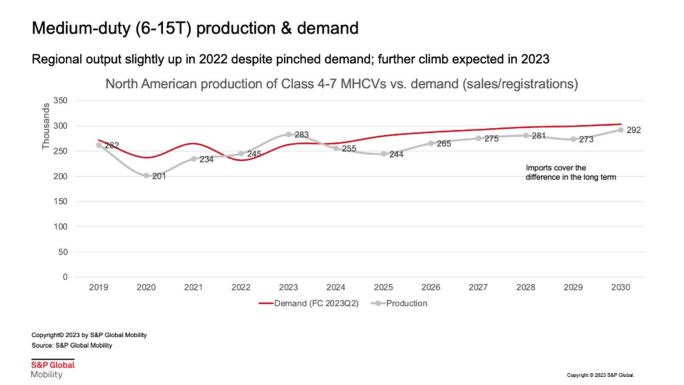

Near-term forecasts from S&P Global Mobility suggest that the post-pandemic market corrections will flatten demand and growth for Class 5-8 commercial vehicles in North America.

However, introducing new regulations in 2027 is expected to drive accelerated growth through electrification.

Despite initial concerns, the US economy avoided a significant recession in 2023 due to resilient consumer spending on durable goods and nominal goods.

The recovery of services, travel, and restaurants has also provided a boost to freight and truck activity.

However, supply chain issues stemming from the aftermath of the COVID-19 pandemic continue to constrain progress.

As we approach the fourth quarter, a slowdown is anticipated, likely to persist into 2024, resulting in a period of soft growth for the industry.

Reduction in Medium-Duty Vehicles in Q2 2023

S&P Global Mobility's Q2 2023 forecast update suggests a moderate reduction in demand for medium- and heavy-duty commercial vehicles in the coming years, following a strong first half of 2023.

However, the updated forecast maintains a more positive outlook for 2025 to 2026 as the industry prepares for the next level of emissions regulations.

Anticipation of the third tier of greenhouse regulations in 2027, combined with the timing of fleet replacement cycles, is expected to drive a wave of pre-emptive buying and bolster demand during that period.

While the overall momentum may slow, the forecast estimates a dip in demand to around 505,000 units in 2024 (including buses and motorhomes), with projections indicating an increase to approximately 543,000 units by 2025.

The transition to cleaner energy in the trucking sector, mainly initiated in California and other states following CARB regulations, is expected to support volume growth in 2023 and beyond.

In addition to anticipated new-product updates, both established manufacturers and startup OEMs are introducing "cleaner" versions of their existing truck models, such as Freightliner's eCascadia, Hino's XL8 series, and Paccar's Kenworth and Peterbilt BEV models, which comply with zero-emissions standards.

Medium-duty (6-15T) production & demand

Photo: S&P Global Mobility

Market Trends in Vehicle Classes

There are several variations in observable market trends across different vehicle classes:

Class 4 trucks, which were popular until the beginning of 2022, have been increasingly taken as lighter-duty applications for last-mile distribution during the pandemic. Ford's Class 4 Econoline Cutaway model accounts for nearly two-thirds of models in this segment and may see increased competition rising from the start-ups entering the fray.

Class 5 vehicles, while facing supply chain issues, are expected to see an increase in demand following a post-pandemic pause - for example in public-sector buying.

Class 6 trucks have gained attention due to their fuel efficiency and suitability for many commercial purposes. However, softening of the housing and construction market triggered a dip in Class 6 truck registrations.

Class 7 trucks have declined in popularity due to their licensing requirements and higher costs than Class 6, in addition to the recent preference of OEMs and customers for trucks that bracket this segment.

After a stronger 2022 where OEMs focused on Class 8 trucks amid supply chain bottlenecks, we expect tractor-truck registrations to remain flat this year before a dip in 2024, and a modest upward trajectory picks up again starting in 2025.

New Laws Forcing Traditional OEMs To Re-Evaluate

Regardless of weight class, the more stringent environmental compliance will be the key driver in demand and production of all vehicle types.

Upcoming regulations, specifically the proposed greenhouse gas emissions standards by the Environmental Protection Agency are forcing traditional OEMs to re-evaluate their manufacturing and investment strategies and prompting a potentially rapid shift from internal combustion engine (ICE) products to electrified vehicles.

In conjunction with the continued push for more aggressive decarbonization efforts by states like California with its Advanced Clean Fleet regulation, these laws act as the key catalyst in the transformation of powertrain technologies.

However, the transition to hydrogen and fuel cell technologies remains limited by cost, infrastructure, and availability issues. This suggests battery-powered electrification as the go-to strategy will be pushed further into the midterm until those issues can be resolved – notwithstanding the recharging network for BEV trucks, which remains to be built.

Looking Toward 2024

Brands like Tesla and Nikola will accelerate this transition for their part and help strengthen the US as the region's epicenter of production.

As for the legacy brands, despite supply chain and labor issues, their Class 4-8 production rates for the North America region reached and even slightly exceeded the average build rates of 2019 by the end of 2022. While some production targets are still not being achieved, inventories continue being rebuilt – setting the stage for potential growth later.

"Inventory figures of Class 4-7 trucks - which represent about half the market - remain below long-term averages, which is one reason why we think production has some upward potential," said Andrej Divis, executive director of global truck research at S&P Global Mobility.

Overall, present demand is still strong, owing to the muted risk of recession compared to the previous two quarters, combined with surprisingly resilient consumer activity. Production is expected to sustain its surge in the short term, while remaining constrained by supply chain and labor issues, before levelling off and even declining in 2024.

More Vehicle Research

Electrification Incentives: The Acquisition Windfall Fleets Can't Miss

Discover how fleets can use tax credits, grants, rebates, and vouchers to dramatically reduce electric truck and charging infrastructure costs—before today’s funding disappears.

Read More →

Top 50 Executive Fleets

It is that time of year again! Time for the 2026 list of the Top 50 Executive Fleets, presented by Automotive Fleet and Volvo as part of its annual Fleet 500. Download now to see this year's list of companies!

Read More →

Back at Star Nation for a Closer Look at Western Star Trucks and the People Behind Them

Work Truck returned to Western Star’s Star Nation Experience for another hands-on look at the trucks, technology, and operator community behind the brand.

Read More →

The Top 300 Commercial Fleets

The Top 300 Commercial Fleets: See the List

Read More →

Mack Defense Receives Additional Order for 115 Heavy Dump Trucks Under U.S. Army’s M917A3 Program

The latest order of 115 Heavy Dump Trucks (HDTs) from Mack Defense for the National Guard is part of the $47-million order from the U.S. Army approved in the 2026 National Defense Appropriations Act.

Read More →

Rizon Introduces Service Combo Body, Increases Electric Truck Applications

Rizon now offers a combo service body that combines lockable storage and a spacious cargo bed in a single zero-emission vehicle. The body supports unique options including cranes, ladder racks, generators, lift gates, and work lighting for a wide range of vocational applications.

Read More →

MFTBC Establishes FUSO Academy Dubai Training Center to Strengthen Network Capabilities in Middle East & Africa

Mitsubishi Fuso Truck and Bus Corporation’s new FUSO Academy Dubai Training Center will support technical and non-technical capability development. It features enhanced training infrastructure to improve service quality, uptime, and readiness for advanced vehicle technologies.

Read More →

Paccar Updates MX-11 and MX-13 Engine Software to Enhance Customer Operations

Kenworth Truck Company and Peterbilt Motors Company will update software for vehicles equipped with Paccar MX-11 and Paccar MX-13 engines to ensure they comply with EPA guidance on diesel exhaust fluid inducements.

Read More →

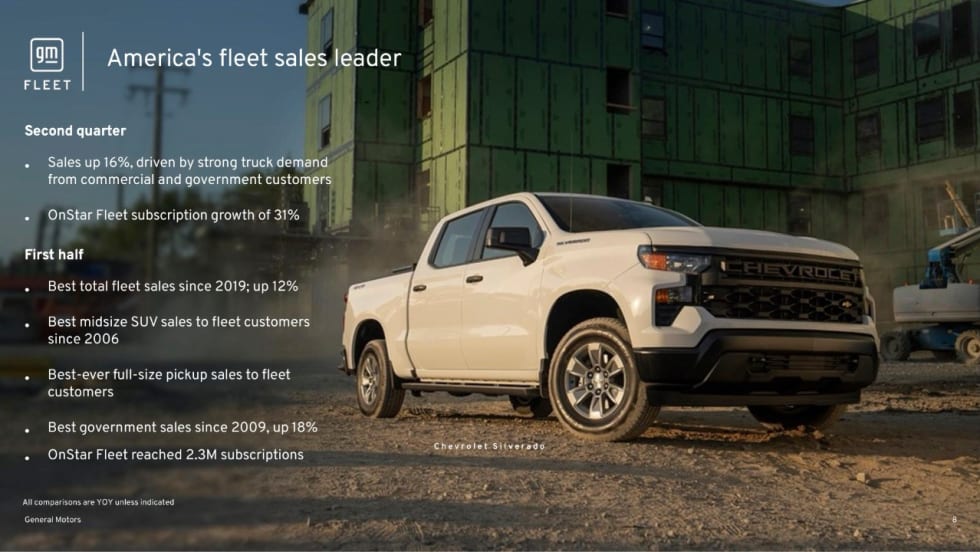

GM #1 in U.S. Sales for the Second Quarter of 2026

General Motors said it was America’s #1 automaker in U.S. sales for the second quarter of 2026 with total sales of 714,896 vehicles, down 4.2%. GM led in full-size pickup and large SUV sales and reported growth in fleet sales.

Read More →